Mortgage For Rental Property: Step by Step Guide - New

Whether you are a novice working on your first property, a veteran hunting down your tenth home, or you are searching for a high-rise apartment building, most investors will begin their journey at the same place: securing a mortgage for rental property investments.

Unless you’re drowning in investment capital, you will need to convince a bank that you can pay back a sizable sum over a few years; and even if you can afford to buy your investments outright, sometimes there are benefits to getting a rental property mortgage instead. After all, by getting a mortgage for rental property investments, you can stretch your finances much further.

I can tell you first hand from my own experience as an investor that getting a good mortgage for rental property investing is absolutely essential to long-term success in real estate.

That is a big part of why I started LendCity, so that I could build a team to help investors like you get the best rental property mortgages possible. So, if you would like to learn more about how my team can help you get the best available mortgage for rental property investing, just book a call at the link here and we can get started.

Residential or Commercial Financing?

The first question to ask yourself is the kind of mortgage for which you will be applying. That means deciding if you’re after a residential mortgage or a commercial mortgage.

When seeking out an investment property, single-family homes and multi-unit buildings up to 8 units are eligible for residential loans. (Yes I said 8 units, this depends on the province of your investment ) Anything larger than that and you’ll be pushed into the world of commercial loans.

That's not to say that one option is necessarily better than the other. There are clear advantages to both residential and commercial rental property mortgages.

When you secure a commercial loan, potential financiers look at the expected performance of your property as a key metric. In a residential loan, your income is the highest priority.

However, commercial mortgages typically take longer, require a higher down payment and have higher interest rates than residential loans, but they make up for it in their flexibility. Unless of course you are using CMHC for your insured purchase of an apartment building. In that case the down payments can be much lower than traditional mortgages with longer amortizations.

Download your FREE Printable Excerpt for this Step By Step Guide

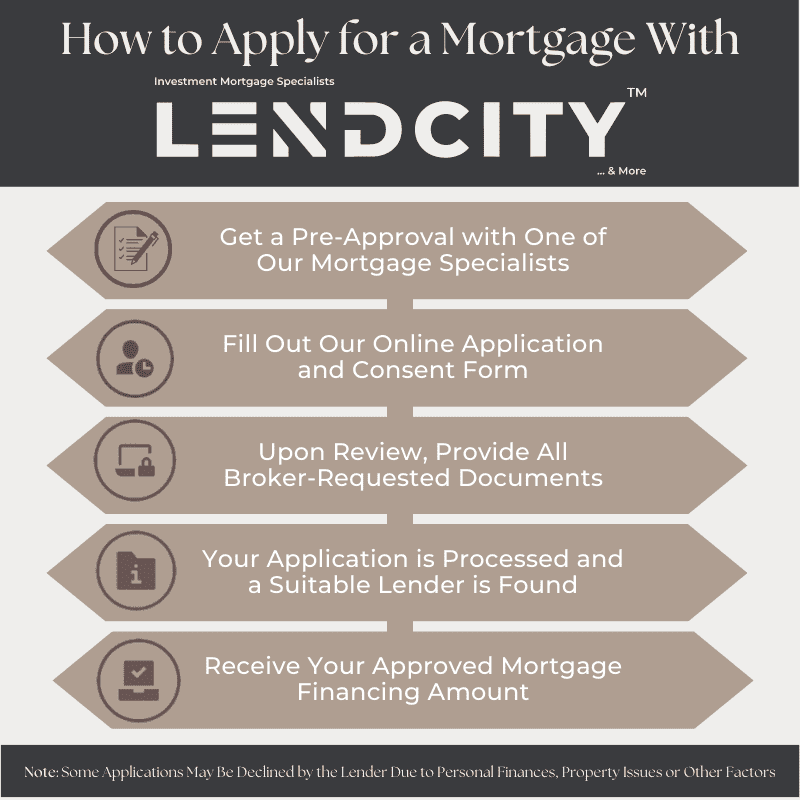

Head to a Mortgage Broker

Even if you already have an established relationship with a bank, your best bet to secure any type of loan is to head to a mortgage broker. The primary reason to pick a broker over a bank is flexibility. When you head to a bank, they are limited to selling their products at their rates. This means that the best product for you may not even be available at your bank.

On the other hand, a mortgage broker works with a variety of lenders - including major banks - so that you can be confident that you can find the best available mortgage for rental property investing no matter which lender it comes from. Also, going to just one bank your limited to how many rental properties you can purchase, where, if you go with an investor friendly broker you can purchase unlimited rental properties.

Think of it like this: going to a bank is like walking into an Apple store. You can’t walk up and down the aisles and expect to find a Microsoft product. You’re only getting Apple computers. Going to a broker, on the other hand, is like heading to Best Buy. You’re going to see several products from several different manufacturers, which leaves you free to choose the best option for your needs.

If you are looking for a mortgage broker, I have great news for you! I operate my own mortgage brokerage. At LendCity, my team and I are committed to helping you secure the ideal mortgage for rental property investing and more. If you would like to hear about my team can help you get the best strategic financing available, book a call with us here.

Consider Getting a Pre-Approval

Before you locate the building you wish to purchase, it’s worth contacting your mortgage broker to get pre-approved for a residential or commercial investment loan. The reasons for this is three-fold:

Requesting pre-approval gives you an idea of which documentation you’ll need to collect and show to secure a mortgage without the hassle of a tight timeline.

Dealing with a financial institution will help you determine your budget’s ceiling before you go off and make an offer without all the information.

Knowing that you are backed by a financial institution that is willing to leap with you will give you the confidence to bid the moment you find a building you love and see potential in.

I also find that pre-approvals can help you make informed purchases. With one in hand, you already know exactly how much you can afford to buy before you ever enter the market.

Lastly, the pre approval really allows us to structure your application for success. To keep growing your portfolio, you must apply in a strategic order with the lenders. Of course if you have elevated debt ratios the order may change by how much rental income the lender will use on your application. Most lenders only use 50% of the rent, however, you may need to partner with a lender that will use 80% or even 100%.

Where Will You Be Living?

If you’re considering the purchase of a multi-unit building, you should determine if you’ll be taking up residence in the building itself. If you’re trying to secure a commercial loan, that question doesn’t matter.

However, if you will be buying an apartment building with four or fewer units, that puts you into the realm of a residential mortgage. In that case, you’ll want to seriously consider the benefits of living in your rental property.

If you’re living in a building with 2 units, resident landlords need only put down five percent of the building’s value as a down payment. If the building you buy has four units, you have to put down 10 percent as a down payment if you’re living there. This is because while you are buying a rental, the property is still your principal residence. That makes it eligible for all the same benefits that you would get buying your own home.

If you won’t be residing on the property however, you will need to come up with 20 percent or more as a down payment for the property.

Finding the Right Property

Did you know that the specific details of a property can play a role in its financing?

There are plenty of factors to consider when buying a property that mortgage lenders will want to look at that can majorly change the status of your application.

Notably, lenders care a lot about location. There are certain lenders who will only finance properties in major cities or properties within a certain distance of their offices.

There are also certain locations that some lenders will not touch at all due to insurance, safety and marketability reasons. This includes properties next to a gas station, properties along train tracks, and properties too close to the shoreline.

So, if you want to go with a certain lender or a certain type of lender, you may want to ask your mortgage agent what to avoid.

Alternatively, if you want a specific property, you should ask your mortgage expert if they work with a lender that will still finance the deal.

Get to Know the Rules and Regulations

Even after your purchase a property, your lender may have certain rules and regulations as part of their financing agreement that you will need to follow.

Some common restrictions include not being allowed to use the property as a student house/rooming house, not being allowed to use the property as a short-term rental, and requiring you to live on the property if your mortgage was meant for principal residences.

Every lender has their own rules, but that is why your mortgage agent is there to help you navigate each lender and their restrictions so that you can find the best product for you.

Filing the Application

Once you have taken everything into consideration and worked with your mortgage agent to ensure that everything is in order, it is time to apply with the lender.

However, it is important to note that sometimes even if you are already pre-approved with one lender, another lender may have a better product available once it is time to actually get a mortgage.

Fortunately, if you are working with a mortgage broker and not applying directly through a bank, they will be able to match your application with the best product for you regardless.

From there, all you need to do is provide the right documentation and follow instructions as given by the lender and your agent and you should be on your way.

Documentation

After your application is complete, your lender is going to reach out to you for paperwork that is needed to verify the application.

Supplying your documents can be the most challenging part of the whole process for an investor.

However, don't take this personally. A lot of rules have been created and established by other clients trying to beat the system, or committing fraud.

The lender is not your enemy, even though it can feel like it. However, lenders will need to confirm everything thats on the application.

One of the main reasons for being so thorough is the lenders get audited by governing financial bodies. If the lender fails an audit they could face a large fine. The profit from a mortgage is not worth the fine the lender faces.

Why Should You Get a Mortgage for Rental Property Investing?

For some investors, getting a mortgage is a necessary part of buying property. Real estate is an expensive endeavor and you cannot expect people to always have the cash on hand to buy their investment properties outright.

However, even if you can afford to buy a property in cash, there are still clear advantages to securing a mortgage for rental property investments.

The first reason is liquidity, you want to have money on hand for things such as property renovations, marketing, furnishing and more. If you spend all of your money buying a property, you may not be able to get the full value out of a rental.

Secondly, making consistent mortgage payments can help you build your credit score and improve your financial standing. While you may pay more in the long run due to interest payments, it will pay off in the form of improved credit and higher financial standing.

Finally, getting a mortgage allows you to do more with your money. If you have the option to buy a property for $500,000 in cash, that same money could go towards up to five properties with a $100,000 down payment each if you wanted to secure mortgage financing instead. In the investing space, this is call scale. You want to scale properly to attain the largest portfolio.

If you would like to learn more about how using a mortgage for rental property investing can help you make more strategic investment decisions, book a strategy call with me and my team and let us show you.